The allocated resources could not mitigate the financial and administrative crisis currently faced by the company, but they had a high opportunity cost; that is, public investment alternatives with an impact on welfare and closing gaps were left unexecuted to favor the company’s bailouts.

According to estimates from the Peruvian Institute of Economics (IPE), from 2013 to date, the cost generated to the State by the financial support to Petro-Perú would have reached S/32.1 billion. Of this amount, 62% (S/19.94 billion) would have been recorded during the terms of former presidents Pedro Castillo, Dina Boluarte, and José Jerí.

What projects or interventions could have been financed with these funds? The amount allocated in the last four years would have allowed, for example, to finance seven times the combined budget of the social programs Juntos and Pensión 65 or 12 times the modified budget of the National Scholarship Program (Pronabec) planned for this year [see infographic].

Carlos Casas, former Deputy Minister of Economy and researcher at the Research Center of the University of the Pacific (CIUP), stated that with these resources it would have been possible to execute 40% more public investment throughout the country. The specialist emphasized important gaps such as citizen security and food security.

“The security budget could have been doubled. When you look at the security budget, it represents approximately S/9 billion. Doubling or even multiplying this amount by 2.5. We could also have quadrupled the budget to protect early childhood development. And this includes the issue of anemia,” he explained.

Martín Valencia, head of economic studies at IPE, highlighted that with an amount of almost S/20 billion, 260 high-performance schools could have been built, 77 medium-complexity hospitals implemented, or 18 times the budget of just the Juntos program financed, which costs more than S/1 billion.

Just the enabling of a financing line of US$2 billion (equivalent to about S/6.8 billion) with State guarantee approved in Urgency Decree 003-2026 issued on May 11 would have covered 58% of the transfers necessary for the 10.4 million poor and extremely poor Peruvians to overcome this condition for one year (S/11.866 billion). In the case of the latter, the amount would have been sufficient to lift them from extreme poverty to a “non-poor” situation, according to an estimate by the Network of Studies for Development (Redes).

Read more 2026 Elections LIVE: check the latest news on Keiko Fujimori and Roberto Sánchez ahead of the runoff

Paola del Carpio, research coordinator of this entity, told El Comercio that this amount would have an immediate impact on enabling health services and educational scholarships.

“With the last bailout of US$2 billion, you could rebuild the entire first level of care type I-4 and almost half of the type I-3 facilities. Currently, more than 95% of your first-level care facilities are in poor condition,” she said.

Uncertain future

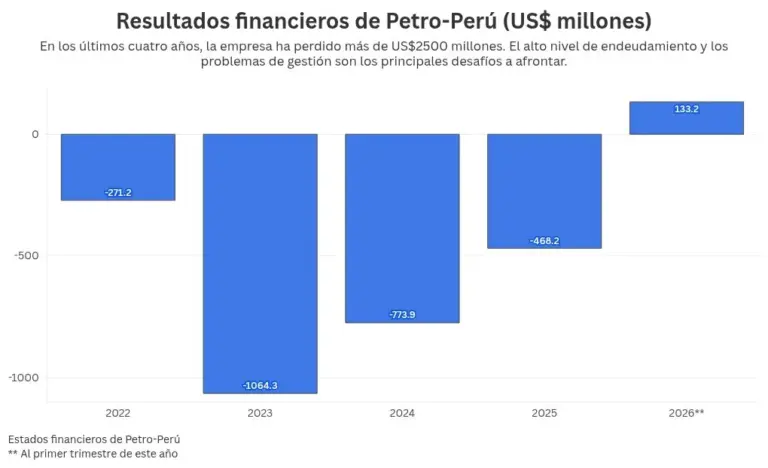

Despite the new transfer, specialists highlighted that the recent resources would only serve to cover debts and short-term payments to suppliers. According to the company’s financial statements, at the end of the first quarter of 2026, the company reported profits of US$133.2 million. In the last four years, it accumulated consecutive losses of more than US$2.576 billion. Currently, its total debt is almost four times its equity.

“You have a Flexi Coking unit that allows refining quite heavy crudes into lighter fuels that is not operating at 100%, for example, and requires repair. That is in addition to the short- and long-term debts that Petro-Perú has,” Valencia asserts.

“One understands that it is necessary not to completely stop operations. But [the transfers] cannot continue without an end date; we have been bailing out for a long time in exchange for nothing. Privatization is often confused with this entry of private capital management,” Del Carpio opines.

The last bailout to the company occurred when the Ministry of Economy considered requesting a supplementary credit of S/11 billion to guarantee subnational elections and complete public works in regions. “A supplementary credit of this amount is approximately 0.8% of GDP. This is based on the mistaken assumption that revenue will continue to grow at high rates. You end up managing fiscal accounts always at the limit of deficit targets instead of thinking about achieving a surplus to rebuild the fiscal stabilization fund,” Valencia said.

- Petro-Perú: Its president says no to the forensic audit of the Talara refinery, why would the new officials be refusing?

- The real turning point at Petro-Perú is not financial

- ProInversión reveals it has already received investor proposals for the Talara Refinery